[ad_1]

Introduction

The Tax Cuts and Jobs Act (“TCJA”), passed in December of 2017, enacted an important provision that has provided significant changes to the treatment of research and experimental (“R&E”) or research and developmental (“R&D”) expenditures under Internal Revenue Code (“IRC”) Section 174. Under the TCJA, for amounts paid in tax years beginning after December 31, 2021, United States-based R&E expenditures must be capitalized and amortized over a 5-year period, while foreign R&E costs, defined as expenses incurred outside of the U.S. based on the location the activities took place, must be capitalized and amortized over a 15-year period.

Prior to the TCJA, taxpayers had the option to immediately expense their R&E expenditures (the default option), choose to ratably deduct R&E expenditures over a 60-month period, or make an annual election under Section 59(e) to amortize R&E costs over a 10-year period.

IRC Section 174 expenditures defined

IRC Section 174 expenses are costs incurred in connection with a taxpayer’s trade or business that represent research and development costs in the experimental or laboratory sense. U.S. Treasury regulations define these costs as generally including all such costs incident to the development or improvement of a product1.

Discovering information to eliminate uncertainty in the development of a product

The regulations further articulate that costs represent R&D expenditures if they are for activities intended to discover information that would eliminate uncertainty pertaining to the development or improvement of a product, which refers to any pilot model, process, formula, invention, technique, patent or similar property, and includes products to be used by the taxpayer in its trade or business, as well as products to be held for sale, lease or license2.

Defining uncertainty

Uncertainty exists if the information available to the taxpayer does not establish the capability or method for developing or improving the product or the appropriate design of the product. Such costs that are incurred and categorized as Section 174 spend may be incurred after production begins, but before uncertainty concerning the development or improvement of the product or process is eliminated.

Identifying types of expenditures included in the scope of Section 174 requiring capitalization

While it is difficult in practice to clearly identify Section 174 costs by the definition provided by the U.S. Treasury, we do have a definition of what it is not.

Specifically excluded from Section 174:

- Costs incurred to acquire land or other property used for mineral exploration.

- Depreciable property (i.e., capital equipment, buildings, etc.) is not subject to Section 174, but the depreciation expense under Section 167 on such property used in R&D can be.

- Ordinary testing or inspection of materials or products for quality control.

- Efficiency surveys, management studies, consumer surveys, advertising or promotions.

- Acquisition of a patent, model, production or process.

- Research in connection with a literary, historical or similar project.

Specifically included for Section 174:

The TCJA amendments to Section 174 stipulate that software development expenses paid or incurred in tax years beginning after December 31, 2021, will no longer be deductible under Rev. Proc. 2000-50; rather, all software development expenditures will be treated as R&E expenditures under Section 174, and therefore, must be capitalized.

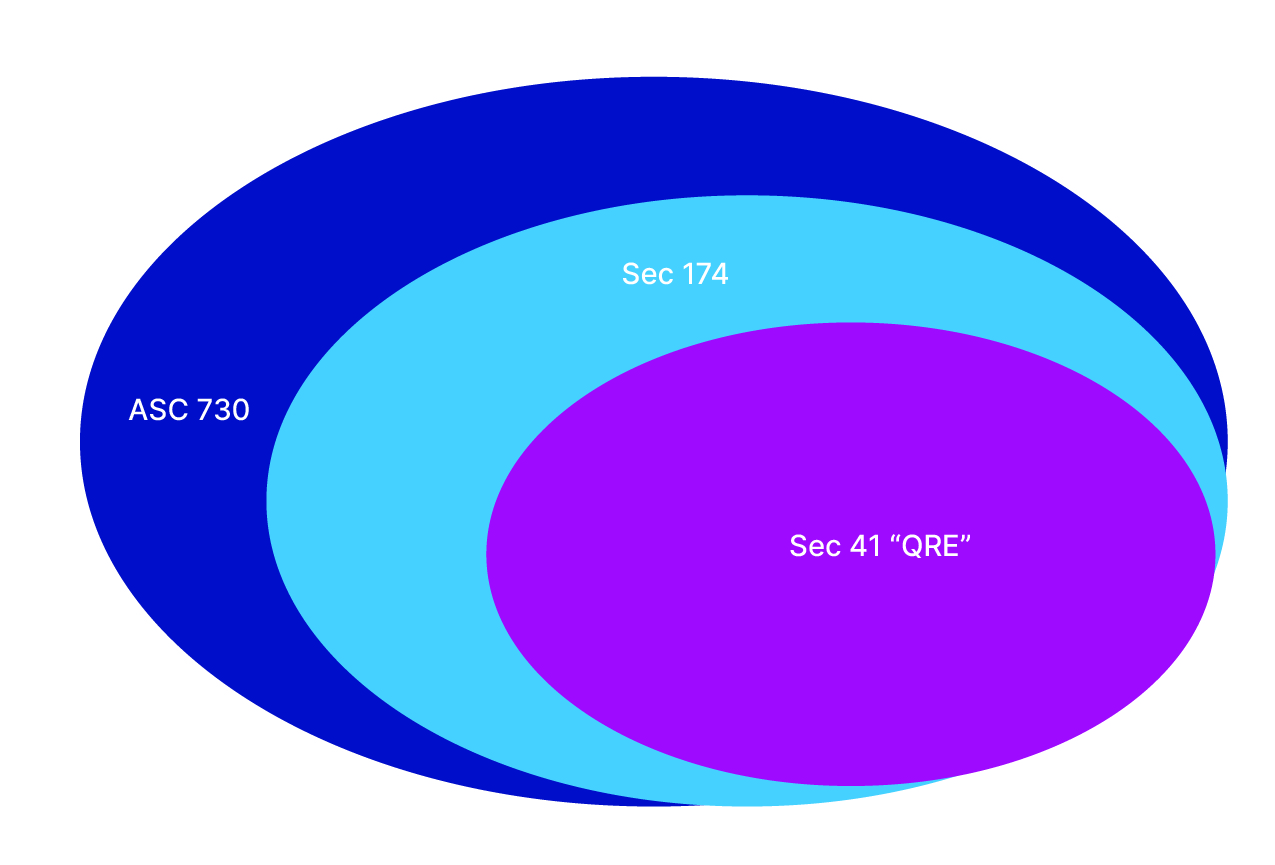

As a practical matter, taxpayers would normally use their financial statement classification of research and development costs as the starting point in determining their R&D expenditures for tax purposes. However, the criteria for categorizing generally accepted accounting principles (GAAP) R&D expense (ASC 730), and software development costs to be capitalized for GAAP (ASC 350-40), are not the same as identifying Section 174 R&E costs. Furthermore, simply equating GAAP R&D to Section 174 costs could lead to significant errors when attempting to report the correct amount of capitalized costs on a tax return.

GAAP – As a general concept, ASC 730 costs are those that are expensed immediately for book purposes and tend to be “all-encompassing” because management often includes all costs incurred within entire R&D departments without any granular analysis. ASC 350-40 costs are designated capitalizable internally developed software costs strictly for feature development and improvement activities. GAAP costs would normally include both direct costs (e.g., wages and contractor expenses), and allocated overhead costs. In addition, shortcuts may be employed using an average salary (e.g., product department and engineering department), which is then applied to the number of R&D hours spent.

Section 174 compared – Under the “specified research” definition provided by Section 174, ASC 350-40 costs would generally be capitalized for tax purposes, but would only represent a small portion of the total amount capitalized for tax since the definition of “incidental costs” is much broader than the ASC 350-40 requirements. However, Section 174 costs tend to be less than ASC 730 costs, but may include costs that exist outside of R&D book expense (e.g., technical support groups or certain IT functions).

Generally, R&E expenditures include all costs incident to the development or improvement of a product or process, including, but not limited to, the following cost categories:

- Wages paid to employees directly involved in R&E activities

- Wages paid to employees incidentally involved in R&E activities

- Payroll taxes

- Supplies

- Contracted research (above the 65% limit required by Section 41)

- Computer lease expense

- Licenses

- Rent

- Depreciation

- Utilities and other overhead costs

- Legal fees

- Travel costs

It should be noted that Section 174(d) provides that if capitalized Section 174 costs are disposed of during any year in which amortization is permitted, no deduction of the capitalized costs is allowed during that year, and the costs will continue to be amortized.

BPM insights:

When faced with the issue of what to do about capitalizing Section 174 costs, the best place to start is to speak with the taxpayer’s external auditor and determine what their expectations are in terms of calculation detail. If there is little impact on the financial statements due to significant built-up net operating losses, a taxpayer and their auditor may be comfortable with a high-level approach that leverages GAAP R&D or a departmental cost inclusion approach.

Hybrid approach

The auditor may permit the use of a “hybrid approach,” where the detail from an R&D tax credit study could be utilized as a starting point as expenses eligible under Section 41 for the R&D credit are most likely also Section 174 costs3. This provides a possible shortcut to identifying the largest costs, such as wages, supplies, contract research and computer lease expenses. One may then look to the trial balance or general ledger to identify and include additional required costs, such as rent, utilities, depreciation, legal fees, etc. It is important to note that if an R&D tax credit study is leveraged, foreign research costs will not be included as “qualified research” under Section 41 and will have to be recognized and captured separately for capitalization purposes. In addition, it should be noted that only 65% of contract research costs are included for the purposes of an R&D credit study. Section 174 requires 100% of relevant contract costs to be capitalized.

Taxpayers who do not have audited financial statements or R&D tax credit studies for the current or prior years may need to find a practical approach. This often means starting with the company’s trial balance and identifying anything that may be coded as R&D before performing additional research.

Practical approach

If a taxpayer does not have detailed GAAP R&D costs and instead has general and administrative (G&A) costs and R&D costs comingled together, then there should be a practical approach undertaken to separate the combined costs between Section 174 costs and otherwise non-capitalized costs. As noted, Section 174 cost categories generally include wages, payroll, supplies, contracted research, overhead, IT, software licenses, etc. To find a practical solution, it may be necessary to allocate such costs on a headcount basis (e.g., a ratio of R&D employees to total employees) or use some other ratio that can be documented and supported to produce a reasonable answer. Without further guidance from the Internal

Revenue Service (IRS), documenting the approach taken will be of the utmost importance to protect the taxpayers’ position in the case of an IRS examination.

Business component approach

There is also an opportunity to be very granular with the analysis and review the Section 174 costs from a “business component” perspective to fully vet whether the entire business component meets the Section 174 criteria of demonstrating “activities intended to discover information that would eliminate uncertainty” and applying a “shrink back” to the Section 174 costs of the component4. This could be an opportunity for certain taxpayers to mitigate the amount for Section 174 costs that require capitalization. It is worth noting that applying the so-called “shrink back” analysis to software development costs may prove much more difficult due to the plain language5 of Section 174 under the TCJA.

Funded research

Another important issue that may arise is with respect to “funded research.” Funded research activities are conducted by the taxpayer on behalf of a third party. In instances where the taxpayer does not have an “economic risk of failure” (meaning the taxpayer being funded will not have to repay the funding party if the results of the research efforts are not fruitful), there could be an argument that the activities they are performing for the third party are service-related and may not be considered as Section 174 costs. These costs may instead be categorized as Section 162 and perhaps should not be capitalized. This is not a definitive position and should be evaluated with the assistance of a technical expert.

Industries affected

Companies such as those in the life science, product innovation, aircraft and computer industries, which are traditionally R&E heavy, are clearly affected by the capitalization requirements as discussed above. As are those companies that seemingly don’t traditionally have R&D spend (e.g., service industry, real estate, retailers, hospitality and construction) but may still have capitalization requirements if they develop their own software. All companies need to start with the question: Does any of their spending have an element of uncertainty?

Other thoughts

To date, the IRS has yet to provide specific guidance for how practitioners are meant to identify and capitalize Section 174 costs; as such, the effort to do so could be viewed as an estimate for purposes of financial statement reporting. The ASC 740 FIN 48 financial statement impact and disclosure thereof would need to be evaluated. R&D credits claimed, and any resulting FIN 48 amounts associated thereof, should be compared and contrasted to the Section 174 capitalized amounts on an annual basis.

BPM has invested extensive resources in developing certain metrics that can be used as a basis for an estimate or benchmark. These metrics measure the results of analyses that compare a Section 41 study to GAAP costs in arriving at Section 174 capitalization.

Foreign research implications

U.S. multinational corporations often conduct R&E activities in their controlled foreign corporations (“CFC”) to improve U.S.-owned intellectual property (IP), compensating them on a cost-plus basis. In these situations, the U.S. multinational must generally capitalize the Section 174 amounts paid to the foreign corporation (which may represent the entire cost-plus payment) over a 15-year period, based on the performance of these activities outside of the U.S. Generally, where the CFC does not own the IP, but is merely performing the R&E activities or “funded research” on behalf of the U.S. parent company (if the parent owns the IP), the CFC would not normally be required to capitalize the R&E expenses incurred.

However, when a CFC owns the IP, any Section 174 costs incurred by the foreign corporation (for R&E performed outside of the U.S.) related to that IP must be capitalized by the CFC and amortized over a 15-year period. In instances where the foreign corporation owns the IP, but pays the U.S. for R&E activities, the foreign corporation would capitalize these expenses and amortize over 5 years (for R&E performed in the U.S.), but the U.S. corporation would not be required to capitalize the R&E expenses incurred. The U.S. corporation may, however, be entitled to R&D credits. Note that where a cost-share agreement (“CSA”), defined under Section 1.482-7, is in place, each party to the CSA possesses some rights in the IP. Consequently, the respective parties would capitalize the proportionate share of the R&E cost as determined based on the reasonably anticipated benefits (“RAB” share).

Conclusion

Navigating the Section 174 capitalization rules is challenging, especially for those new to this code section. The rules are complex and require a thorough understanding of both tax law and the specific R&E activities being conducted by the business. BPM’s National Tax group and Specialized Tax Services team are available to help. We have dedicated specialists currently working with our clients to navigate these complicated rules and support their calculations. Contact us for more information.

1 Treasury Regulation 1.174-2(a)(1)

2 Treasury Regulation 1.174-2(a)(1) and (3)

3 IRC Section 41(d)(1)(A) – the term “qualified research” means research with respect to which expenditures may be treated as specified research or experimental expenditures under section 174.

4 Treasury Regulation 1.174-1(a)(2) Application of section 174 to components of a product. If the requirements of paragraph (a)(1) of this section are not met at the level of a product (as defined in paragraph (a)(3) of this section), then whether expenditures represent research and development costs is determined at the level of the component or subcomponent of the product. The presence of uncertainty concerning the development or improvement of certain components of a product does not necessarily indicate the presence of uncertainty concerning the development or improvement of other components of the product or the product as a whole. The rule in this paragraph (a)(5) is not itself applied as a reason to exclude research or experimental expenditures from section 174 eligibility. 5 Section 174(c)(3)

[ad_2]

Source link